Menu

A merchant cash advance (MCA) is a type of relatively quick and easy business financing. MCAs are easy to get but typically have exceptionally high interest rates and fees that can significantly affect profitability until they are repaid. In addition, daily or weekly withdrawals from a business’s operating account are required, severely hampering a company’s cash flow. Small businesses are particularly tempted by MCAs when they need to make ends meet temporarily. If you are a business owner, be sure you understand the disadvantages and advantages of a merchant cash advance before you apply for one.

A merchant cash advance pays you or your company a lump sum in cash against future sales. The business receives a lump sum payment deposited into the business bank account.

The financing company charges a fee called a factor rate, rather than an interest rate. The factor rate is used as a multiplier for the amount of the loan to determine the repayment amount. For example, a $50,000 MCS with a factor rate of 1.5 would cost a total of $75,000, plus potential additional fees charged by the financing company, such as an origination fee, underwriting and/or funding fee, and an administrative fee.

Repayments are either daily or weekly and are usually withdrawn from the bank account of the business. The repayment amount may be a percentage of credit and debit card sales, called a holdback, which usually ranges between 10 and 20 percent of revenue. Alternatively, the repayments may be a fixed withdrawal amount; in this case, the repayment term is predictable, but the business does not have the option to extend it if revenue slows down.

If you default on a merchant cash advance by missing a payment, the MCA company can either sue you or execute on a confession of judgment that you were required to sign as part of the application for the MCA.

Merchant cash advances have both advantages and disadvantages. A business owner must make certain to understand both the pros and cons before applying for an MCA.

An MCA can provide immediate access to cash. Almost any business with ongoing receivables can qualify, even one with bad credit. In many cases, the business does not have to provide collateral, since repayment is guaranteed by future revenue.

The aggressive repayment schedule of daily or weekly repayments continues until the advance is fully repaid. The factor rate and fees translate into interest rates often far in excess of interest rates on conventional business loans. Our firm has seen many of these “loans” have an effective interest rate well in excess of 100% annually. Since MCAs are structured to attempt to avoid qualifying as a business loan, they sometimes are not subject to loan usury laws that establish maximum interest rates and other loan laws and regulations. Litigation over this very issue is going on in bankruptcy courts today.

The repayment schedule may seem manageable for the business owner initially, but it can turn into a cash flow nightmare due to the unpredictability of future sales. Ultimately, a business can end up in a never-ending borrowing cycle that leads to ever-increasing costs, which can jeopardize continuation of the business.

In some cases, the MCA company requires the business owner to make a personal guarantee, which puts their private assets at risk, or execute a confession of judgment that waives the owner’s right to defend against a court action. Those terms make default (non-payment) of a merchant cash advance more onerous than default on a conventional business loan.

When a business takes out an MCA, there is no advantage to repaying early, unlike many traditional business loans. The business must pay the full repayment amount, regardless of when the MCA is paid off.

Because an MCA does not qualify as a business loan, a business cannot build credit through MCA financing. Repayment history is not reported to the credit bureaus.

If you are a business owner considering a merchant cash advance to alleviate financial concerns, it is critical to explore available alternatives for traditional and conventional business loans instead of taking out an MCA. The exceptionally high fees and costs of an MCA, the burdensome terms in the event of a default, and the potential never-ending debt cycle are overwhelming disadvantages that can spell the end of a business in a short period of time.

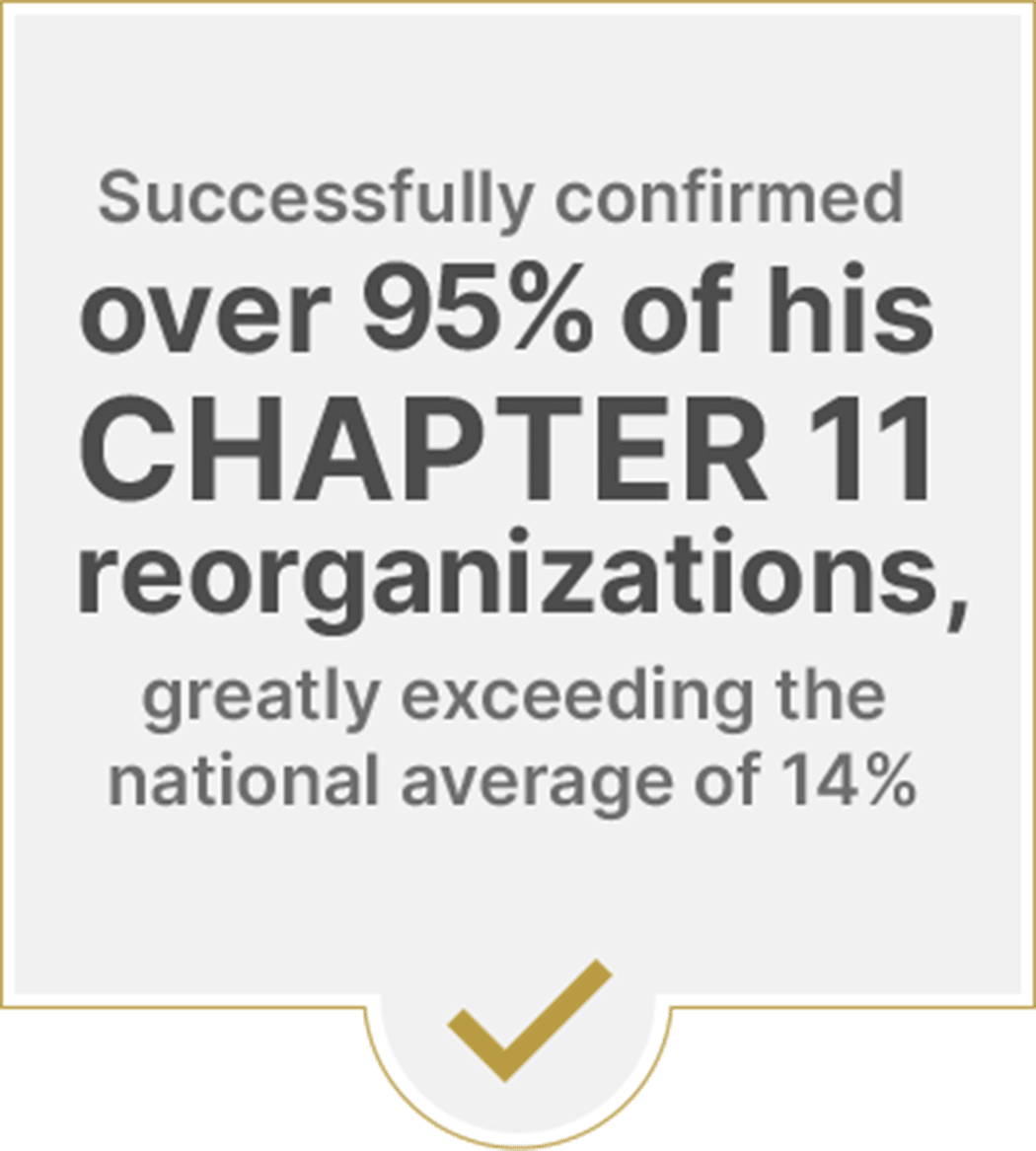

If you already have financial issues because of merchant cash advances you previously took, bankruptcy may be an option to alleviate your financial difficulties. Depending on the circumstances, Chapter 7 business liquidation, Chapter 11 business reorganization or small business bankruptcy under Chapter 11, Subchapter V may be viable options.

Connect With an Experienced Florida Chapter 11 Lawyer

At Wernick Law, we focus our practice primarily on Chapter 11 debtor representation. We welcome Florida businesses wishing to learn more about Chapter 11 reorganization bankruptcy or Subchapter V, Chapter 11 small business reorganization to schedule a consultation by calling 561-961-0922 or using the online contact form.

Based in Boca Raton, Wernick Law serves clients in South Florida (including West Palm Beach, Broward County, and Miami), Southwestern Florida (including Naples and Fort Myers), Tampa, Orlando, Jacksonville, and elsewhere in the state.

© 2026 Wernick Law, PLLC

| View Our Disclaimer | Privacy Policy